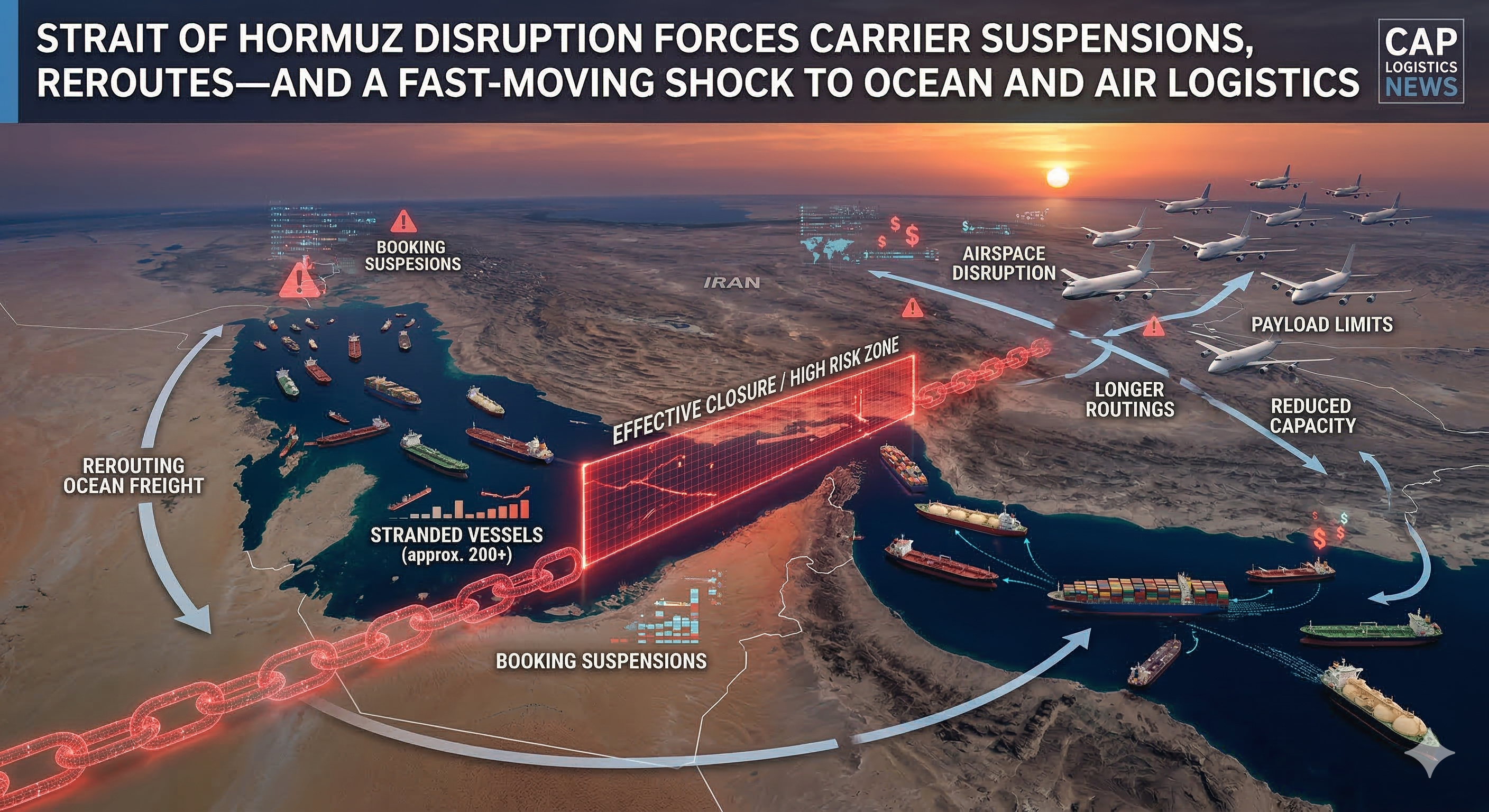

Security escalation around the Strait of Hormuz is producing an “effective closure” pattern: carrier booking suspensions and cargo-type limits, vessel backlogs, and air cargo reroutes that reduce reliability across key trade corridors.

- MARAD and UKMTO/JMIC advisories since Feb. 28, 2026 have elevated operating risk across the Strait of Hormuz and surrounding waters.

- Major carriers have issued service restrictions, including limits on dangerous/special cargo and reefers, and are advising alternative routings.

- Lloyd’s List reported roughly 200 compliant tankers stranded as traffic through the chokepoint froze, raising delay and demurrage risk.

- Gulf airspace instability is also impacting long-haul air cargo networks through longer routings, payload limits, and reduced schedule reliability.

- Operational conditions remain fluid and port-by-port; planners should assume higher variance in transit time and contract execution risk.

A rapidly escalating security situation around the Strait of Hormuz is triggering widespread operational suspensions and reroutes across ocean freight—and compounding disruption in air cargo corridors that normally traverse Gulf airspace.

Major carriers have issued formal service restrictions, while U.S. and international maritime security bodies have published alerts warning commercial shipping to treat the region as a high-risk operating environment. The net effect is an “effective closure” scenario: even without a universally recognized legal closure declaration, a large share of commercial traffic is avoiding transit due to war-risk exposure, safety constraints, and insurer/charterparty triggers.

What happened (and when)

-

Feb. 28, 2026: The U.S. Maritime Administration (MARAD) said “significant military activity commenced” in the Persian Gulf, Strait of Hormuz, Gulf of Oman, and Arabian Sea, and urged heightened precautions for U.S.-linked commercial vessels operating in the area. MARAD’s alert also directs operators to stay in close coordination with Naval Forces Central Command (NAVCENT) guidance and to consult UKMTO/JMIC products. (MARAD MSCI Alert 2026-001A)

-

Feb. 28, 2026 (UKMTO / JMIC): UKMTO published Advisory 003-26 and subsequent updates citing a volatile security environment and advising vessels to transit with caution and report suspicious activity. The Joint Maritime Information Center (JMIC) also issued an advisory note covering the same escalation window and risk environment. (UKMTO Advisory 003-26 Update, JMIC advisory note PDF)

-

March 2–4, 2026: Multiple carrier advisories moved from “monitoring” to active restrictions. Maersk stated it was suspending acceptance of certain high-risk cargo types (including reefers and dangerous/special cargo) in and out of several Gulf countries “until further notice,” and separately circulated customer documentation referencing the “effective closure” of the Strait and associated surcharges/operational measures. (Maersk Middle East operational update, March 2, Maersk customer PDF, March 4)

-

March 3–5, 2026: Industry tracking and port-operation reporting indicated a steep reduction in transits and a buildup of vessels waiting outside the chokepoint, with some ports experiencing intermittent operational constraints. Lloyd’s List reported around 200 compliant tankers stranded as Gulf traffic froze in the immediate aftermath of the escalation. (Lloyd’s List, March 3, Lloyd’s List ports operational update, March 5)

Who is restricting service—and what that means operationally

Ocean freight: suspended bookings, cargo-type limits, and reroutes

Carrier measures are converging on three concrete outcomes:

-

Booking controls / acceptance suspensions into and out of Gulf gateways (especially for higher-consequence cargo such as dangerous goods and temperature-controlled freight). Maersk’s March 2 notice explicitly suspended acceptance of reefers and dangerous/special cargo across multiple Gulf countries. (Maersk)

-

Service instability on Middle East corridors (schedule blanking, ad-hoc omits, and “alternative gateway” recommendations). Even where ports remain technically open, the combination of security routing decisions, pilotage limitations, and the need to keep crews and vessels out of designated risk areas is undermining reliability.

-

War-risk and insurance mechanics now drive routing. In practice, when operators and masters determine that transit exposes the vessel to war risks, standard contractual clauses can be invoked to refuse unsafe voyage orders—tightening available capacity and pushing shippers toward longer routings or different modes. (See industry legal guidance summarized by Hill Dickinson in relation to the current situation and BIMCO war-risk clauses.) (Hill Dickinson analysis)

Tankers and energy-linked flows: queueing, delays, and price-sensitive knock-ons

The largest immediate chokepoint exposure is energy: crude, refined products, and LNG movements that normally rely on predictable Gulf load windows.

-

Lloyd’s List’s vessel counts and stranded-ship reporting point to rapid congestion and forced waiting patterns rather than orderly, metered transit—an operational condition that can create cascading impacts on product availability, demurrage exposure, and downstream refinery/power generation supply timing. (Lloyd’s List)

-

Separately, analysis circulated via GlobeNewswire citing Wood Mackenzie outlined a scenario in which even a limited-duration disruption could materially reduce LNG availability for South Asia, underscoring the risk of secondary impacts on industrial energy users. (Wood Mackenzie scenario via GlobeNewswire, March 11)

Air cargo: Gulf airspace instability becomes a capacity and reliability problem

While the Strait itself is a maritime chokepoint, the same escalation is also affecting air routes through Gulf airspace, which are integral for Asia–Europe (and some Asia–U.S.) long-haul routings.

-

Logistics providers’ operational updates describe longer routings, higher block times, payload limitations from fuel burn, and reduced schedule reliability as carriers reroute around closed or constrained airspace. (NNR airfreight update, March 6)

-

Trade press has also pointed to measurable reductions in available lift when broad airspace closures occur in the region, amplifying rate volatility and limiting time-definite options for critical parts. (Air Cargo Week, March 2)

What remains uncertain

Several high-impact variables are still moving:

-

Duration and enforceability: Some industry advisories stress there is no universally recognized “legal closure,” yet the operating reality is dominated by heightened threat levels and carrier-level directives that suppress traffic anyway. (ISS Middle East Port Advisory PDF, March 3, MARAD)

-

War-risk designations and labor terms: The ITF and Joint Negotiating Group designated the region as a Warlike Operations Area (WOA), which can affect crewing terms, premiums, and willingness/ability to operate in the zone. (ITF/JNG statement, March 5)

-

Port-by-port operating status: Individual terminals may remain open while pilots, tugs, crew-change permissions, or road access are restricted intermittently—creating a pattern of “open but not fluid.” (ISS advisory PDF)

Practical implications for shippers and project cargo

For industrial supply chains—especially heavy industry, power generation, mining, and construction projects—the immediate planning impacts are concrete:

- Longer and less predictable lead times for cargo touching Gulf gateways, driven by reroutes, acceptance suspensions, and port-window uncertainty.

- Higher probability of force majeure/war-risk clause invocation in chartering and liner service contracts, increasing the importance of clear risk allocation and contingency routings.

- Mode shifts under pressure: Airfreight may not be a clean workaround if Gulf airspace remains constrained; it can become costlier and less reliable at the same time ocean options degrade.

Why this matters to CAP Logistics readers

For CAP Logistics’ industrial and heavy-industry customers, the key near-term action is to treat Gulf-linked routings (ocean and air) as contingency-required: validate carrier acceptance rules by cargo type (DG/reefer/OOG), build schedule buffers for critical spares, and pre-align alternate gateways and insurance/contract terms before cargo is released to execution.

FAQ

Is the Strait of Hormuz legally closed to commercial shipping?

Multiple advisories note there may be no universally recognized “legal closure,” but the operating reality is an effective closure for many operators: elevated military risk, insurer/charterparty considerations, and carrier directives are sharply reducing commercial transits.

What carrier actions are most likely to affect industrial cargo?

The most immediate impacts are booking suspensions or restrictions by cargo type (dangerous goods, special cargo, reefers), service reroutes/omitted calls, and schedule unreliability caused by security-driven operating constraints.

Can airfreight bypass the disruption?

Not reliably. Gulf airspace instability can force longer routings, increase block times, reduce payload due to fuel burn, and cut overall capacity—often raising rates and reducing schedule reliability even for time-critical shipments.

What should project shippers watch in the next 1–2 weeks?

Carrier advisories by lane and cargo type, war-risk area designations and insurance conditions, port-by-port operating status (pilotage, labor, road access), and any changes to UKMTO/JMIC/MARAD guidance that would signal either de-escalation or broader restrictions.